A Chinese-style social credit system is coming to America

Opinion by David Bahr

The ease with which personal banking is conducted in the modern West would surely cause some envy to our mattress-stuffing ancestors. Cashpoint machines abound, plastic is easy to carry, and, most comforting, one’s money is backed by the full faith and credit of the government. Importantly, unless one fundamentally transgresses the legal order, we can be sure our capital is always at a moment’s access.

Put another way, except in cases usually pertaining to national security, banks are rather indifferent to a client’s private life. The good, the bad, and the ugly are all welcome provided they have the right decimal count. And so, it pains me to report that in America, a peculiar phenomenon dubbed “de-banking” is beginning to occur with increasing visibility.

“De-banking” (or “de-risking”) is what it sounds like. A bank will, for legal, liability, or reputational risk, terminate – with notice – an individual account. Normally, this does not grab our attention. Criminal organisations and terrorists, we all agree, should be frozen out. And, of course, banks may choose with whom to conduct business.

Recently over a dozen Republican attorneys general – the main legal advisors to our state governors – wrote a letter to Brian T. Moynihan, the Chairman of the Board and CEO of Bank of America (BOA) noting that the institution “appears to be conditioning access to its services on customers having the bank’s preferred religious or political views.” In a seven-page memo, the attorneys generals outline BOA’s partnership with the Federal Bureau of Investigations and the US Treasury to “profile conservative and religious Americans as potential domestic terrorists.”

The seeming weaponisation of our banking institutions to target Americans guilty of “wrongthink” is of a piece with the targeted censorship from certain behemoths in Silicon Valley. It was not too long ago that the New York Post, a paper founded by Alexander Hamilton, found its reporting on Hunter Biden “limited” by Facebook and Twitter. In effect, this meant that the story would not gain traction on two of the largest news platforms on earth.

Banking, like our modern news consumption, is by and large transacted through a digital medium. If an organisation is “de-platformed” from a webserver or “de-banked,” from, say, the second-largest bank in America, claiming nearly 15 per cent of all domestic deposits, there are not many options left. And that is by design.

So, conservatives should be worried. It was not too long ago that Lois Lerner, head of the IRS’ Exempt Organisations Unit under President Barack Obama, used her power to specifically target conservative non-profits. This clear government malfeasance was met with outrage, and she was forced to resign. The private sector, especially the large banks, are not so easy to take to task. This is a problem.

A strong banking system is built, above all else, on transparency. Opaque account-cancellation policies based on subjective standards of “reputational risk” – whatever that means – not only cut against the spirit of free-enterprise but it super empowers an elite few to control the lives of most citizens. (Ironically, the very same citizens who are forced to provide bailouts to banks like BOA when times get tough.)

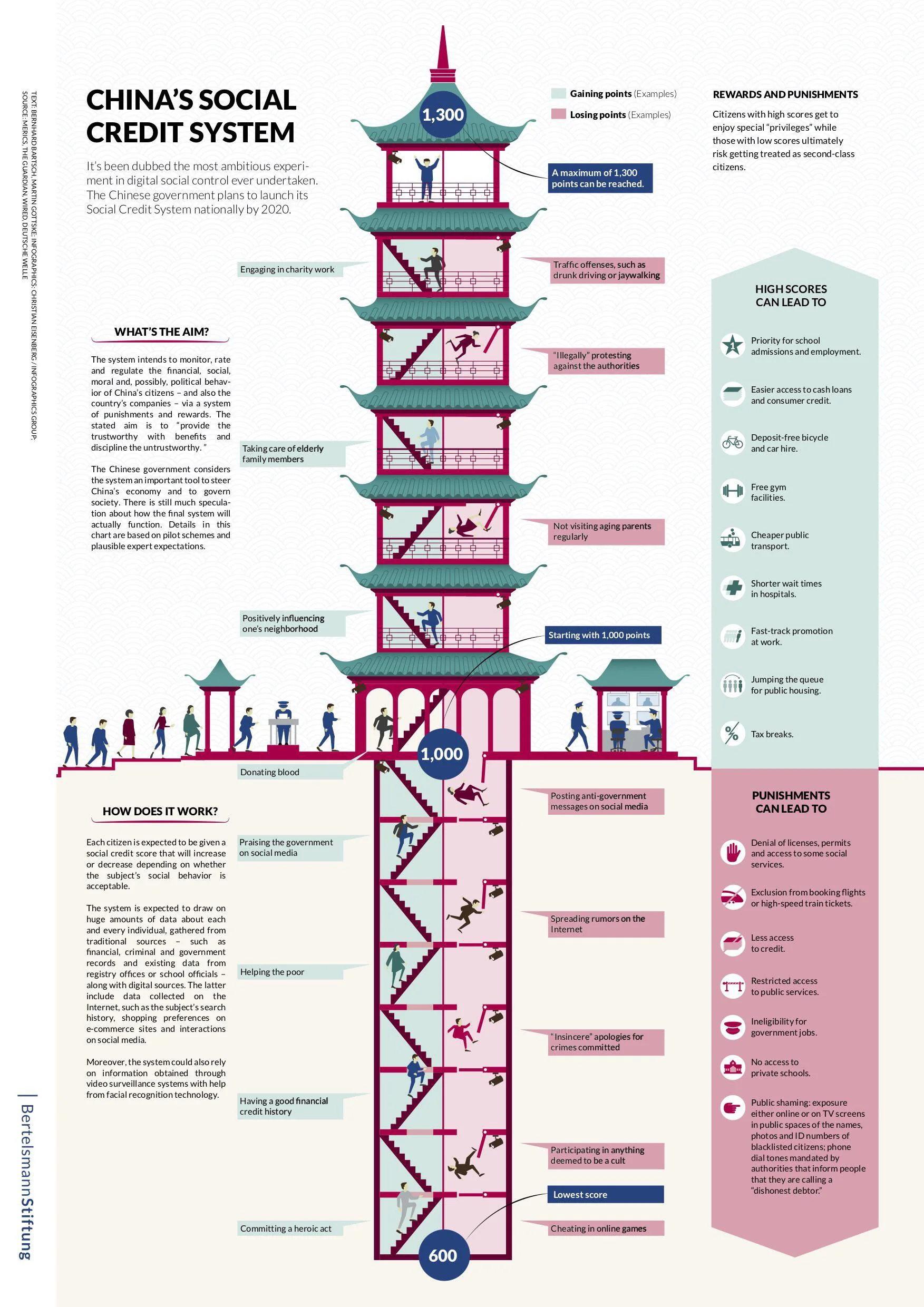

We often scoff at the notion that a “social credit” regime could never happen in America or the UK. This form of tyranny, we believe, is surely not the stuff of democratic regimes devoted to liberty. But it is happening here – with increasing success.

Comments (0)